It is pretty much sold out despite being at a much bigger venue this year, so you can understand that it’s been rather hectic for our brilliant and hardworking team.

Meanwhile, our publishing division is putting the finishing touches to Volume 38 of PV Tech Power, the quarterly journal for the downstream solar PV sector to which Energy-Storage.news contributes the Storage & Smart Power section. It is, of course, included in your subscription to ESN Premium.

A lot to do but more importantly, a lot to look forward to.

But before we get to that, today’s Friday Briefing gives us the perfect opportunity to instead look back on the Energy Storage Summit 2021 and get a fascinating snapshot of where some of us were back then, and what we thought we’d see in the market by, well, now.

It’s unlikely many of us look back on the second year of the global pandemic and the human cost of lives and productivity lost or damaged with great fondness. As a much more minor consideration than that, I expect not many of us miss what was euphemistically described as “the new normal” of cancelled conferences hosted online instead of in person.

But, actually, the industry – and again, the Solar Energy Events team – did a great job even then. One silver lining is that the 2021 edition’s live streamed sessions are all available on the Solar Energy Events team’s YouTube channel.

I was privileged and honoured to be asked to moderate the keynote panel discussion which opened the event, and its participants included representatives from Gore Street Capital and Gresham House. They were at the time, managers of the UK’s two listed funds dedicated to investing in large-scale battery energy storage system (BESS) assets, since joined by Harmony Energy Income Trust to make three.

One of the big topics at that time, which feels pretty relevant to think about today as well, was that the market was mid-shift towards revenue stacks that were more focused on merchant risk than on contracted revenues.

“Generally, from our perspective, we think that it’s true, and it’s definitely going to be the case, that future stacks and revenue streams will be very different for batteries than they are now,” Alicia Kowalewska-Montfort, Gore Street Energy Storage Fund project manager said.

Kowalewska-Montfort referred to a period towards the end of 2020 and beginning of 2021 when huge price spikes resulted in some prices in the market reaching £4,000 (around US$5,500 at that time)/MW/hr. That was, she said, a “small sample” that nonetheless indicated that the direction of travel towards increased renewables on the grid, and therefore increased volatility, would create more and more viable opportunities for storage.

Anyone accurately predicting the business case for BESS assets 20-25 years down the line would have to be a magician or fortune-teller, the project manager said. However, the overall thesis Gore Street held was that wholesale energy trading would play an increasingly large layer of the revenue stack, with ancillary services revenues as the “baseline”.

Gresham House fund manager Ben Guest said that with the growing importance of trading on the horizon, Gresham House was looking to incrementally increase the duration of its assets – which was, of course, referred to as an ongoing piece in the fund’s recent financial update a couple of weeks ago.

“Ultimately, the ancillary services market is much smaller than the deeper energy markets. But I agree with Alicia, which is that it’s difficult to know when trading becomes very profitable,” Guest said.

“There are some very, very good guideposts, which [are from] simply analysing the change in the generation mix, and therefore in the merit order.”

As we heard from Henry Easterbrook of developer Fig Power in our recent webinar on merchant risk, Guest said two years earlier that it’s the fate of natural gas in the Great Britain (GB) electricity market which might most clearly decide just how much battery capacity, and at what duration, will be playing into wholesale markets.

You can watch the opening keynote panel: ‘What is the Key to Really Making Money from Batteries?’ below and you can indeed also watch the rest of the event’s great sessions – and lots of other content – on the event team’s channel here.

It includes lots of great content and speakers, by no means limited to the UK market alone, so we’d highly recommend having a browse.

[embedded content]

We very much hope to see you at next week’s Summit, part of our industry-leading series of global conferences. Look out for news and exclusive interviews from the show in the coming weeks.

In other stuff to look forward to on ESN Premium, join us early in the week for an exclusive interview with advanced compressed air energy storage (A-CAES) company Hydrostor.

Here’s what that article’s author, Cameron Murray, Energy-Storage.news senior reporter, has to say about that:

“The Canada-headquartered company is often described as a compressed air energy storage technology A-CAES firm, but Hydrostor president Norman told us it would be more apt to call it a system integrator and, currently, it’s just as busy doing project development.

The approach is different to most other long-duration energy storage (LDES) technology firms, which tend to just provide technology for other companies’ projects. But, whether it remains that way long-term is an open question, and one Norman discussed for the interview.”

Happy Friday!

Friday recap: This week on ESN Premium

In case you missed them… click the headlines to read the following Energy-Storage.news Premium articles:

Transferability ITC deals for 1GWh+ of US battery storage: ‘market has grown faster than anyone expected’

Blackstone and Foss & Company have completed transferability investment tax credit (ITC) deals for BESS projects in California and Texas, a market that has grown “faster than anyone expected” according to tax credit ecosystem Crux.

sonnen CEO: ‘We gained credibility in the US through Utah virtual power plant’

Utah is not perhaps a US state people would immediately associate with cutting-edge clean energy tech development, but that’s where sonnen’s virtual power plant (VPP) offering took shape.

Illinois BESS project owner seeking damages from LG for ‘defective’ supplied batteries

The owner of a battery energy storage system (BESS) project in Illinois, US, is seeking at least US$10 million in damages from LG Energy Solution for supplying allegedly defective batteries, a court document shows.

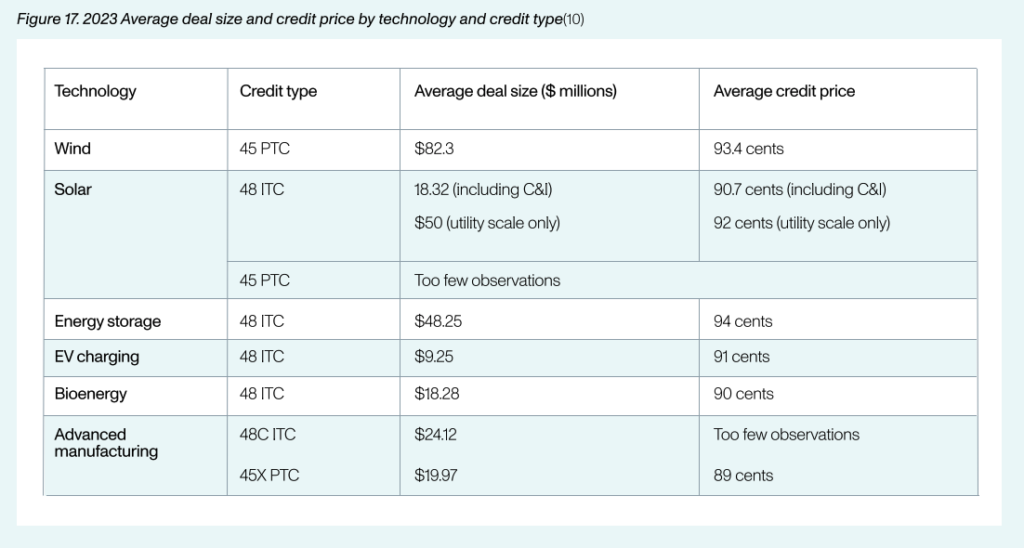

Energy storage tax credits in US priced highest among all clean energy types

Energy storage investment tax credits (ITC) were priced more highly than any other clean energy type in transferability transactions last year, according to a report from tax credit ecosystem Crux which its CEO discussed with Energy-Storage.news.

Continue reading